"It

is impossible for ideas to compete in the marketplace if no forum for

their presentation is provided or available."

Thomas Mann, 1896

Turning Data into Smart

Decisions

Why Business Intelligence is Imperative

for Enterprises

Sponsored by: Microsoft

Corporation

The

Business Forum recently organized a

The

Business Forum recently organized a

Business Forum Luncheon discussion with

Microsoft Corporation at the Saint

Francis

Hotel, in

San

Francisco, California.

Those responding to our invitation included:

CIO

- Alameda

County Information Technology Department * Purchasing

Manager - Blue

Shield of California * Staff

Counsel - California

Department of Insurance * Human

Resources Director -

California Rural Legal Assistance Inc. * Technology

Team Manager - CSE

Insurance Group * Customer

Service Manager - DTIS

- City & County of San Francisco * Vice

President - Fireman's

Fund Insurance Company Director

Counsel - Fremont

Group * Special

Projects Associate - Fremont

Group * President

- Grady

Hicks Enterprises Inc. *

Human Resource Manager – Gensler

Associates * Vice

President, Human Resources - Pacific

Exchange * Publishing

Systems Manager - San

Francisco Newspaper Agency Captain

- San

Francisco Police Department * President

- Sevan

Networks Inc. * Information

Systems Project Manager – San

Francisco Fire Department * Director

for Business Services - Stanford

Linear Accelerator Center * Manager,

Decision Support Systems - Stanford

Linear Accelerator Center * Director

of Human Resources - The

Asia Foundation * President

– Technical

Services Associates Inc. * Finance

Manager - Wells

Fargo Bank, Corporate Properties Group *

For the benefit of those of our

members and supporters who could not

attend the meeting we present the following white paper, with contacts

Bringing

the Balanced Scorecard to Life:

The

Microsoft Balanced Scorecard Framework

Insightformation, Inc.

Contributed

by Microsoft Corporation

White Paper - Published: May 2002

For the latest information, please see http://www.microsoft.com/business/bi/

Abstract

This

paper describes the Microsoft® approach to developing and implementing a

Balanced Scorecard for enterprise performance management. It presents basic

information on the Balanced Scorecard performance management methodology, and

identifies key business issues that must be addressed in developing and

deploying a balanced scorecard. The paper then presents the Microsoft Balanced

Scorecard Framework (BSCF)—a comprehensive set of techniques, tools, and best

practices to speed scorecard implementation using toolsets with which

organizations are familiar.

An

extensive body of research and literature describing the Balanced Scorecard

exists. That body of knowledge is constantly being expanded by The Balanced

Scorecard Collaborative, Balanced Scorecard Institute, various consulting

organizations, software companies, and client organizations. This paper cannot

comprehensively cover such a complex topic or reflect accurately many of the

nuances of scorecard development and implementation. Instead, it presents a

basic conceptual overview of the Balanced Scorecard. Interested readers are

encouraged to use the bibliography presented at the end of this paper as a guide

to more detailed information.

Executive

Summary

Traditional performance measures are insufficient to gauge performance and guide organizations in today’s rapidly changing, complex economic landscape. Organizations need to link performance measurement to strategy, and must measure performance in ways that both promote positive future results and reflect past performance.

The Balanced Scorecard has developed over the last eleven years as a powerful way to implement strategy and continuously monitor strategic performance. Creating a strategy focused organization (the phrase coined by the founders of the Balanced Scorecard methodology) is a significant, challenging culture change for many organizations. Success in achieving this change requires:

Consistent executive support and involvement.

Education, communication, and visibility of the strategy and measurements of its effectiveness throughout the organization.

Constant feedback loops so that strategy is an every-day consideration.

Tools to enable non-technical users to understand the key drivers of the measures.

Translation of the strategy to operational terms so that alignment to strategy and implementation of it occur at all levels of an organization.

Organizations that have successfully implemented the Balanced Scorecard have achieved remarkable transformations in their financial performance, in many cases vaulting to the top ranks in their industry groups.

Many aspects of Balanced Scorecard development and deployment depend on effective use of technology to be successful. Numerous software packages have been developed to help automate the Balanced Scorecard, but it is very difficult to deliver the needed capabilities in a single software package. Therefore, the Microsoft Balanced Scorecard Framework has been developed to allow organizations to:

Develop and deploy a scorecard economically using an existing infrastructure.

Manage and display the data and knowledge pertinent to Balanced Scorecards.

Facilitate analysis of measures so that prompt corrective action can take place.

The framework provides a comprehensive, flexible, cost-effective way to deploy the Balanced Scorecard and deliver superior returns on people, processes, customers, and technologies.

How do we communicate strategy through a complex, multi-faceted, decentralized global organization? How do we align our organization and minimize superfluous activities so that we’re all working efficiently to the same ends? How do we measure the effectiveness of our strategy and its implementation? How do we promote a culture of agility to respond to the rapidly changing business climate we face?

As business leaders wrestle with these questions each day, they confront the reality that, “If you can’t measure it, you can’t manage it.” In other words, effective performance management requires accurate performance measurement.

Leaders also understand that performance measurement itself is not enough. The value of measurement is that it identifies where action should be taken. So, effective performance measurement systems must be able to:

Accurately reflect a business situation.

Guide employees to take the right actions in situations where action is required.

Gauge the effectiveness of those actions.

A performance measurement system, then, is a closed loop system that embodies situational analysis of information, corrective actions, and result evaluation.

The Balanced Scorecard is a proven performance measurement system. It is a comprehensive strategic performance management system and methodology. It is a framework for defining, refining and communicating strategy, for translating strategy to operational terms, and for measuring the effectiveness of strategy implementation.

This paper briefly describes the history, evolution, and key elements of the Balanced Scorecard. It then identifies the critical success factors for a Balanced Scorecard implementation. Finally, it presents the Microsoft Balanced Scorecard Framework (BSCF) as a way to leverage a corporation’s existing investments and capabilities to develop and deploy a scorecard in a timely, cost-effective, scalable, manageable, and reliable way.

The Balanced Scorecard came into being in the late 1980s and early 1990s as a method to help companies manage their increasingly complex and multi-faceted business environments.

Corporations then were faced with a number of challenges. Market share in many industries was vanishing at an alarming rate due to globalization, liberalization of trade, technology innovation, and domestic quality issues. The economy was in transition from product-driven to service-driven. The composition of the workforce was changing, and companies’ workforce needs were changing.

In spite of all these changes, most businesses still relied on traditional measures of performance based on a centuries-old accounting model, which failed to accurately reflect the true health (and future prospects) of an organization. The need for better information to respond to rapidly changing market conditions was obvious.

In response to these stresses, and the shortcomings of traditional financial performance measures, Professor Robert Kaplan and David Norton began to shape the concept of the Balanced Scorecard during a research project with 12 companies in the late 1980s. They understood the limitations of relying too much on purely financial measures. They realized that many of the ways to improve short-term financial performance—such as reducing headcount, and cutting expenses for training, R&D, marketing, and customer service—might be detrimental to the future financial health of the company. Conversely, companies might appear to be doing poorly from a financial perspective because they were investing in the core capabilities that could drive superior future performance. Furthermore, they perceived the limitation of reliance on lagging indicators that convey past performance results, but do not generally provide a reliable indication of future performance.

Kaplan and Norton also perceived that employees throughout a company often did not understand how their role related to strategy and financial measures, leading employees to feel powerless to impact the things that were being measured.

So, Kaplan and Norton introduced the Balanced Scorecard as a way for companies to measure and report performance in a way that balanced:

Multiple perspectives.

Both leading and lagging indicators.

Inward-facing measures, like productivity, and also outward-facing measures, like customer loyalty.

The results of their initial research work with 12 companies were published in 1992 in the Harvard Business Review. Fueled by the positive response to their initial article and successful consulting work, Kaplan and Norton continued to develop the concept of the Balanced Scorecard, and published the book, The Balanced Scorecard in 1996. By that time, the focus of the Balanced Scorecard had evolved from an emphasis on measures and reporting, to a methodology for promoting strategic management of the organization.

As more and more organizations began to embrace and experiment with the Balanced Scorecard concept, a growing number of tools and techniques emerged, building on many of the initial concepts. In 2000, Norton and Kaplan released their second book, The Strategy Focused Organization, which describes that evolution to a broader concept of enterprise strategic management.

The Balanced Scorecard is a dynamic methodology, and the understanding of its potential deepens as Kaplan and Norton proceed with innovative work, such as developing scorecards for support functions like Human Resources and Information Technology (IT).

Empowering the Knowledge Worker

Today, companies face the same pressures as 10 years ago, but in a radically different economic landscape. A new pressure, then barely on the horizon, has revolutionized the way many businesses must operate—the Internet. The Internet’s impact is ubiquitous. Among other impacts, it has lowered entry barriers to many markets; empowered the customer with information and choice; brought new distribution channels; and spawned entire industry sectors around activities such as customer relationship management, supply chain integration, security, and the marketing of information.

The economy has transitioned to what some call the Age of Information—an economy in which Gross Domestic Product is increasingly dominated by services. In this service economy, the knowledge worker has replaced the production assembly line worker as a key factor of production. Knowledge workers use and process data or information, and in collaboration with other workers, create knowledge and take action, thereby increasing value.

This value creation process is predominantly intangible in nature. In 1998, over 75% of the market value of the S&P 500 was captured in intangible assets. Intangible assets, like any other asset, are factors of production that should be used to generate value. These intangible factors of production are used in ways that may be many times removed from revenue generation or cost reduction; they are frequently indirect contributors to production of a product or service. For example, IT investments involve extensive use of knowledge workers and capital, and are a powerful service facilitator with significant impacts on costs and internal and external customer relationships, but rarely are there direct correlations between IT projects and increased revenue or reduced cost.

So, organizational financial performance is increasingly contingent on generating returns on intangible factors of production. Therefore, organizations must apply the knowledge worker’s expertise in ways that serve a defined corporate strategy to achieve a return on that worker. It follows that organizations must both empower the knowledge worker and measure their performance in relation to strategy.

However, organizations are finding it extremely difficult to implement strategy and measure effectiveness of that strategy. According to Fortune Magazine, only 10% of the strategies that are effectively created get effectively implemented. A related finding by Norton and Kaplan is that without the Balanced Scorecard, 85% of executive teams spend less than 1 hour per month discussing strategy. So even when companies invest a lot of time in refining their values, mission statements, and strategic initiatives, those ideas rarely trickle down to truly transform an organization, and the average employee does not have a clear understanding how his or her actions influence ultimate performance measures such as stock price or earnings per share.

The Balanced Scorecard is a proven way to align an organization with strategy, harness knowledge workers’ efforts to strategic ends, and ultimately deliver improved financial returns on employees, technology investments, business processes, and customer relationships.

Elements of the Balanced Scorecard

The Balanced Scorecard is an approach to describing and communicating strategies. It is also a way of selecting performance measures that will drive a unique organizational strategy. Dr. Norton describes the Balanced Scorecard as follows:

“A balanced scorecard is a system of linked objectives, measures, targets and initiatives which collectively describe the strategy of an organization and how the strategy can be achieved. It can take something as complicated and frequently nebulous as strategy and translate it into something that is specific and can be understood.”

Kaplan and

Norton’s Balanced Scorecard describes strategy and performance management from

multiple perspectives. The classic Balanced Scorecard has four perspectives:

|

Perspective |

Key Question |

|

Financial |

To succeed financially, how should we appear to our stakeholders? |

|

Customer |

To achieve our vision, how should we appear to our customers? |

|

Process |

To satisfy our customers and shareholders, at what business processes must we excel? |

|

Learning and Growth |

To achieve our vision, how will we sustain our ability to change and improve? |

Each perspective can be explained by a key question with which it is associated. The answers to each key question become the objectives associated with that perspective, and performance is then judged by the progress to achieving these objectives. There is an explicit causal relationship between the perspectives: good performance in the Learning and Growth objectives generally drives improvements in the Internal Business Process objectives, which should improve the organization in the eyes of the customer, which ultimately leads to improved financial results.

Though there are four basic perspectives proposed, it is important to understand that these perspectives reflect a unique organizational strategy. So the perspectives and key questions should be amended and supplemented as necessary to capture that strategy. For example, a non-profit or government organization would not have the same perspectives as a for-profit corporation.

Objectives are desired outcomes. The progress toward attaining an objective is gauged by one or more measures. As with perspectives, there are causal relationships between objectives. In fact, the causal relationship is defined by dependencies among objectives. So, it is critical to set measurable, strategically relevant, consistent, time-delineated objectives.

Measures are the indicators of how a business is performing relative to its strategic objectives. Measures, or metrics, are quantifiable performance statements. As such, they must be:

Relevant to the objective and strategy.

Placed in context of a target to be reached in an identified time frame.

Capable of being trended.

Owned by a designated person or group who has the ability to impact those measures.

An organization is likely to have a variety of types of measures. Some will be calculated from underlying data. Others will be aggregated index measures that assign different weights to multiple contributing measures. Some are frequently measured and others may only be measured on a quarterly or annual basis.

It is important to balance lagging indicators—which includes most financial measures—with leading indicators—areas where good performance will lead to improved results in the future.

It is also important to balance internal measures, such as cost reduction, injury incident rates, and training programs, with external measures like market share, supplier performance, and customer satisfaction.

An initiative is a change process or activity designed to achieve one or more objectives. The initiative is what will move a measure toward its target value. Initiatives may be large or small in scope. They generally are owned by a person or group, and are managed like projects.

Strategy Maps, Strategic Themes, and Matrices

Since even a relatively simple scorecard can contain an overwhelming amount of information, several tools have been developed to help communicate large, complex quantities of information in simple, easily understood ways.

Strategy Maps

Mapping a strategy is an important way to evaluate and make visually explicit an organization’s perspectives, objectives, and measures, and the causal linkages between them. Organizing objectives in each defined perspective, and mapping the strategic relationships among them, serves as a way to evaluate objectives to make sure they are consistent and comprehensive in delivering the strategy.

The strategy map is a visual way to communicate to different parts of the organization how they fit into the overall strategy. It facilitates cascading a balanced scorecard through an organization, because it can be created at different levels of an organization, and each level’s map can be viewed for alignment with the overall strategy map.

Figure 1:

Example Strategy Map

Strategic Themes

The strategy map in Figure 1 shows a strategic theme. The strategic theme is a grouping of similar objectives and their measures across perspectives. It helps make a complex strategy more understandable by organizing and categorizing objectives and measures. It also reduces the amount of information and number of causal linkages that need to be drawn on a strategy map. A complex organization might have several strategic themes, with objectives and measures designed to gauge the effectiveness of the organization in pursuing those themes.

Strategy Matrix

The strategy matrix is another useful visualization and summarization tool. It displays objectives, measures, targets, and initiatives in one table. The strategy matrix can point to areas where scorecard elements might be out of balance. For example, there may be a cluster of initiatives around one objective, while other objectives have no supporting initiatives. This can be useful when prioritizing spending for projects. Typically, the strategy matrix will reflect a strategic theme, so one matrix is prepared for each theme

|

|

Strategic Theme: Smart, Profitable Expansion |

|||

|

|

Objective |

Measure |

Target |

Initiative |

|

Financial

|

Increase %

of revenue from new stores

|

% Revenue

from stores opened in last 3 years

|

> 30%

year 1

> 50%

year 3

|

Marketing

to new target markets

|

|

Avg. # of

days to breakeven

|

< 180

days year 1

|

Operations

review

Site

selection

|

||

|

Increase

sales efficiency

|

Revenue per

FTE

|

> $ X

year 1

> $ Y

year 3

|

Self-service

checkout pilot

|

|

|

Customer

|

Acquire new

locations

|

Avg. #

daily customers

|

> X in

first 6 mos.,

> Y in

first year,

> Z by

year 3

|

Local

marketing/PR campaigns

|

|

# of repeat

customers

|

> X in

first 6 mos.,

> Z by

year 3

|

Customer

loyalty program

|

||

|

Avg. $

customer purchase

|

> $ X

year 1

> $ Y

year 3

|

Coupon

program

In-store

promotions & classes

|

||

|

Process

|

Fact-based

site selection

|

Days lag

between market selection and site acquisition

|

< 90

days year 1

< 70

days year 3

|

GIS mapping

National

brokerage contract

|

|

Streamline

development process

|

Project

duration, site acquisition to opening

|

< 365

days year 1

< 300

days year 3

|

Standardize

design/build processes

|

|

|

% stores

open on schedule

|

> 93%

year 1

> 95%

year 2

|

Web-based

project management

|

||

|

Learning

& Growth

|

Use

business intelligence systems

|

% eligible

employees trained

|

>90%

year 1

>99%

year 2

|

In-house

system training

|

|

Integrated

knowledge management

|

# paper

forms used

|

< 200

year 1

< 100

year 2

< 5 year

3

|

Corporate

digital nervous system

|

|

Figure 2: Example Strategy Matrix (for the Strategy Map shown in Figure 1)

Critical Success Factors for BSC Development

Extensive research and evaluation of hundreds of Balanced Scorecard implementations has been done by the Balanced Scorecard Collaborative (the consulting organization established by the founders of the Balanced Scorecard methodology) and various other practitioners. A consistent theme emerges from this body of knowledge: the Balanced Scorecard is a cultural change initiative. Successful organizations use the Balanced Scorecard to create a culture of continual focus on strategy formulation, measurement, and revision. They create what Kaplan and Norton call a strategy focused organization.

The key elements in creating this strategy focused organization are as follows:

1. Mobilize change through executive leadership. Building a strategy focused organization usually involves significant culture change. Organizational change is an evolutionary process. Consistent executive leadership, involvement, active sponsorship, and support are critical to maintaining momentum through the challenges that organizations inevitably encounter.

The executive team must be in agreement on strategies and must drive the scorecard process for it to be successful. Often executives are too busy to be intimately involved in the process, so a cross-functional team is formed. This can be successful if:

The executive team has first participated in facilitated sessions at which the fundamental mission, vision, and strategic themes are established.

The team has the ear of the leadership and can readily escalate issues to executives for resolution.

Executives continue to communicate their support for, and involvement in, the Balanced Scorecard initiative.

2. Make strategy a continual process. A strategic focus is not maintained if strategy formulation becomes a one-time activity. Feedback loops are needed to constantly focus attention on and reevaluate the strategy and the measures. To support strategy evaluation, tools for reporting and analysis should be deployed to enable analysis of the factors influencing the measures. The budget process also is often linked to strategy, and in some cases the Balanced Scorecard replaces traditional budget formulation as a way to allocate funds.

3. Make strategy everyone’s job. This is done through strategic education and awareness and by cascading the scorecard down through the organization, so that business units, departments—or even individuals—create their own scorecards. The linkages to strategy are explicitly defined at all levels. This helps departments and individuals understand and find new ways to support the strategy of the organization. It also helps ensure that employees at all levels are being measured and compensated in ways that support that strategy.

4.

Align the organization to the strategy. This involves

evaluating current organizational structures, lines of reporting, and policies

and procedures to ensure that they are consistent with the strategy. It can

include re-alignment of business units or re-defining the roles of different

support units to make sure that each part of the organization is lined up to

best support the strategy.

5.

Translate the strategy into operational terms. Tools like the

strategy maps, cascaded scorecards, and strategy grids are used to integrate

strategy with the operational tasks that employees perform daily. This ensures

that tasks are done in ways that support the strategies.

When Kaplan and Norton’s second book, The Strategy Focused Organization was published, the Harvard Business Review hailed the Balanced Scorecard as one of the most significant contributions to management practice in the last 75 years. However, despite its well-publicized successes, the majority of organizations that adopt a scorecard fail to reap the rewards they expect. In researching these disappointments, some common themes stand out:

1. Measures that do not focus on strategy. A common problem is that an organization will adopt some new non-financial measures, but fail to align the measures adequately with strategy. According to Dr. Norton,

“The biggest mistake that organizations make is thinking that the scorecard is just about measures. Quite often they will develop a list of financial and non-financial measures and believe they have a scorecard. This, I believe, is dangerous.”

For example, in one case a bank’s IT department had identified measures and benchmarks for being a world class IT department. According to those measures, they had done very well. However, the measures used by the IT department were not tied in with the overall business strategy and therefore discouraged the IT department from meeting the strategic business needs.

2. Failure to communicate and educate. A scorecard is only effective if it is clearly understood throughout an organization. Frequently, scorecards will be developed at the executive level, but not communicated or cascaded down through an organization. Without effective communication throughout the organization, a balanced scorecard will not spur lasting change and performance improvement.

3. Measures tied to compensation too soon. It is generally a good idea to tie compensation to the Balanced Scorecard. However, several factors suggest it can be a mistake to do that too early in the lifecycle of the scorecard.

Rarely is an initial scorecard left unrevised. So, if an organization ties compensation to measures that are not in fact driving desired behavior, a powerful motivator has been instituted that will drive an unwise action.

Data may be incomplete or inaccurate, so measures may not be correct. If employees’ paychecks are adversely impacted, serious morale problems and invalidation of the scorecard inevitably result.

It may take time to determine realistic targets, and penalizing people for failing to achieve an unreachable target will surely have a negative impact on morale and eventually profits.

4. No accountability. Accountability and high visibility are needed to help drive change. This means that each measure, objective, data source, and initiative must have an owner. Without this level of detailed implementation, a perfectly constructed scorecard will not achieve success, because nobody will be held accountable for performance.

5. Employees not empowered. While accountability may provide strong motivation for improving performance, employees must also have the authority, responsibility and tools necessary to impact relevant measures. Otherwise they will resist involvement and ownership. Resources must be made available, and initiatives funded, to achieve success. Employees are likely to need new information tools to help them understand the drivers of measures for which they are responsible so they can take action. These tools can include systems for analysis and early warning indicators, exception reports and collaboration.

6.

Too many initiatives. Large, decentralized organizations

usually find that crossover and duplication among initiatives can be identified.

Cross-matching scorecard objectives with current and planned initiatives can be

an important way to focus and align a company. This method will identify cases

where objectives are supported inappropriately. Rather than relying on budgeting

for strategic funding, this process eliminates waste, speeds scorecard

implementation, and helps an organization prioritize their initiatives to better

support their strategy.

Automating the Balanced Scorecard

A successful BSC program relies extensively on data, education, and communication to promote, monitor, and reinforce behavior modifications—all processes that can be facilitated easily by information technology.

Automation is essential in order to manage the vast amount of information related to a company’s mission and vision, strategic goals, objectives, perspectives, measures, causal relationships, and initiatives. The alternative is a manual process, which significantly increases the effort and cost of scorecard development and sets back progress in the early stages of the BSC development, when momentum is critical.

Automation can foster quicker culture change, both during development and in the ongoing use of the BSC. If the software used is intuitive and can be deployed through an organization readily, it can bring visibility to the BSC process, ease a cultural transition, and enable participation by a wider audience.

A number of software development companies have sought to develop an automated solution and capitalize on the success of the Balanced Scorecard. Various approaches to BSC automation exist, depending on the orientation of the software company:

Proprietary business intelligence (BI) products. One class of scorecard automation software has formed around proprietary BI software products. BI software is designed to support an organization’s reporting and analysis needs. Naturally, a BI software vendor will see the BSC as an extension of BI, and so will develop it as an add-on to their product line. While these packages can meet some of the analytical needs that support a balanced scorecard, they tend to have several limitations:

They can lead an organization to focus on measures derived from available data rather than strategic objectives.

They do not generally provide needed capabilities with regard to strategy communication and managing non-numeric information like reasons for selecting a specific measure.

They often have per-seat license costs that may be appropriate for a smaller number of advanced analytical users but can be cost-prohibitive for the widespread deployment that is needed to drive effective strategy execution.

ERP-centric applications. Another class of BSC software is designed by Enterprise Resource Planning (ERP) software companies to interface with their transactional systems and to try to combat the common perception that their reporting capabilities are unduly limited. These ERP-centric applications tend to emphasize use of the ERP system’s data and may not be as well suited for integrating external data. Due to a heavy database orientation, they generally do not provide ways to manage the unstructured content that is key to educating and communicating with a large employee population. They also usually have per-user costs that can discourage broad use.

BSC-specific applications. The BSC-specific applications generally offer a good presentation layer, but may be limited in their ability to integrate multiple data sources and to enable automation of data collection and transformation. Without integrated analytic capabilities, users may not be able to drill down to more actionable information under the high-level metrics. These applications are often stand-alone applications that don’t easily integrate with existing systems or infrastructure.

These three classes of scorecard automation approach all have significant weaknesses in their ability to support the important processes of education, communication, collaboration, and knowledge sharing that ultimately determine the success or failure of a Balanced Scorecard initiative.

The Microsoft Balanced Scorecard Framework has been developed to overcome these shortcomings.

The Microsoft Balanced Scorecard Framework

The

goal of the Microsoft Balanced Scorecard Framework (BSCF) is to empower an

organization to use the Balanced Scorecard to achieve returns on people,

processes, customers, and information technology. The BSCF is designed to

facilitate scorecard development and deployment at all phases and levels of an

organization—to achieve the benefits of early automation without the attendant

risks.

The

goal of the Microsoft Balanced Scorecard Framework (BSCF) is to empower an

organization to use the Balanced Scorecard to achieve returns on people,

processes, customers, and information technology. The BSCF is designed to

facilitate scorecard development and deployment at all phases and levels of an

organization—to achieve the benefits of early automation without the attendant

risks.

The framework is not a packaged application. Instead, it integrates a variety of Microsoft packaged applications and industry standards to automate a Balanced Scorecard. It consists of a set of tools and methods to help both business users and developers get to success faster and more reliably so software is no longer a hurdle to overcome in scorecard development, but an asset to speed development.

Recognizing the wide-ranging challenges, impact, and needs of an organization implementing the BSC, the BSCF is founded on several underlying concepts:

1. The business and technology requirements for successful scorecard automation are too complex to be bundled into a single package. To be successful, the Balanced Scorecard must be woven into the fabric of an organization. Scorecard automation tools also must be spread throughout the organization. Further, systems to facilitate Balanced Scorecard implementation will necessarily rely on links to existing systems.

2. It is necessary to leverage existing capabilities and technologies. Introducing new software typically entails significant training costs over and above the cost of the software itself. The BSCF exploits existing Microsoft software—already part of most organizations’ software arsenal—to speed adoption and reduce culture shock.

3. An open framework is essential. Organizations should be able to leverage existing systems and can add capabilities when and where needed. There are some specific capabilities for the Balanced Scorecard, or generic performance management, that are not provided as out-of-the-box functionality in Microsoft products. Therefore, these capabilities have been developed using the standard Microsoft development tools with which most IT departments already have experience.

The three underlying principles dictate a holistic, multi-faceted approach to a Balanced Scorecard initiative—an approach that facilitates education, communication, collaboration, analysis, and integration with daily work activities. The BSCF leverages the expertise of Balanced Scorecard practitioners and moves beyond the restrictive capabilities of much early scorecard automation software to address the issues organizations commonly confront. Six facets describe the BSCF:

Personalized Portal

Best Practices

Strategy and Metric Management

Business Intelligence

Actionable and Operational Tools

Knowledge Management

Experts

cite communication and education as two of the most critical success factors in

a Balanced Scorecard initiative. Research has shown that most organizations need

improved vehicles for education and communication in order to succeed in change

processes. In addition, as organizational development specialists know, changing

culture is easier if accomplished in ways that are integrated with, and

facilitate, daily work tasks.

Experts

cite communication and education as two of the most critical success factors in

a Balanced Scorecard initiative. Research has shown that most organizations need

improved vehicles for education and communication in order to succeed in change

processes. In addition, as organizational development specialists know, changing

culture is easier if accomplished in ways that are integrated with, and

facilitate, daily work tasks.

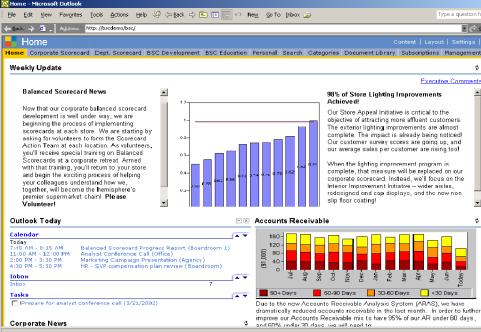

Therefore, the Balanced Scorecard Framework provides a personalized portal for employees. The portal is, in essence, a doorway into the employee’s work life. Built using standard Web technologies, the portal may be easily personalized to accommodate organizational and individual preferences. It can provide links to tools used daily, such as e-mail, calendars, and Web-enabled interfaces to transactional systems. The portal also presents Balanced Scorecard information in manageable pieces to facilitate learning. This learning process is sequenced so that employees learn according to a plan established by the scorecard implementation team.

Figure 3: Personalized Portal Integrating Balanced Scorecard

The portal is introduced early in a scorecard implementation, when it initially serves as a way to communicate and educate. As scorecard development proceeds, the portal provides a dual perspective of overall corporate performance and individual performance.

If an organization already has a portal, the Balanced Scorecard can be implemented within that portal, to leverage the organization’s existing investments.

The portal

becomes habit-forming as the interface between the employee, the performance

management system, and daily work tasks. It provides a link to all other facets

of the BSCF.

The

Balanced Scorecard promotes a fundamentally different way of developing

objectives and measures. Developing balanced, leading, and strategy-focused

measures is a complex task. Organizations—even those that already have a

culture of performance—find they often need guidance to transition their

culture toward a strategy focused organization. It makes sense to take advantage

of the best practices in Balanced Scorecard development—to learn from

others’ experience. Therefore, the framework includes educational components

to facilitate a scorecard development and implementation process.

The

Balanced Scorecard promotes a fundamentally different way of developing

objectives and measures. Developing balanced, leading, and strategy-focused

measures is a complex task. Organizations—even those that already have a

culture of performance—find they often need guidance to transition their

culture toward a strategy focused organization. It makes sense to take advantage

of the best practices in Balanced Scorecard development—to learn from

others’ experience. Therefore, the framework includes educational components

to facilitate a scorecard development and implementation process.

Figure 4:

Best Practices

These components include:

Microsoft PowerPoint presentations for educating employees, which can be viewed using Web technologies.

Links to useful information, such as relevant Web sites, to help teach the balanced Scorecard team, and to educate the organization’s general population.

Process guidelines, answers to Frequently Asked Questions, and mistakes to avoid.

A series of templates for capturing complete data on measures, objectives, perspectives, initiatives, and so on, so that a scorecard implementation team can consistently gather and share the information that must eventually be managed in a Balanced Scorecard database.

Best practices documents are created in standard Microsoft Office products—such as Microsoft Word, Microsoft Excel and Microsoft PowerPoint®—which generally means no software acquisition or employee training is required. These documents are readily convertible to Web formats for display.

Facet

3: Strategy and Metric Management

An

organization implementing a Balanced Scorecard will generate many different

scorecards at the corporate, divisional, departmental, and perhaps even

individual level. Managing the details about strategies, objectives, measures,

and targets is complex. Each measure may have different owners, data

definitions, reasons why it was chosen, and so on. In addition, scorecard

development is a living, iterative process; measures and objectives are

constantly in flux as an organization evolves.

An

organization implementing a Balanced Scorecard will generate many different

scorecards at the corporate, divisional, departmental, and perhaps even

individual level. Managing the details about strategies, objectives, measures,

and targets is complex. Each measure may have different owners, data

definitions, reasons why it was chosen, and so on. In addition, scorecard

development is a living, iterative process; measures and objectives are

constantly in flux as an organization evolves.

Once measures are identified, the data must be acquired. Where possible, data should automatically be pulled from underlying systems or from a data warehouse. This minimizes human error in data handling, and eases the burden of maintaining the scorecard measures at various levels of an organization. However, in some cases, data will not exist in those sources and will need to be entered manually.

Organizations need an efficient, systematic way to collect, sort, summarize, and disseminate all the data that feeds into the scorecards. The BSCF provides this needed functionality with an application that consists of a Microsoft SQL Server™ database and an intuitive Web-based interface for business and technical users. This component application, Scorecard Builder™, conforms to the specifications established by Kaplan and Norton’s consulting organization, the Balanced Scorecard Collaborative, so data can be readily exchanged with other Balanced Scorecard automation packages.

The impact of a scorecard depends to a great degree on the effective display of performance information. Information must be presented in an easily understandable way, using appropriate data presentation techniques. The BSCF includes several Web-enabled presentation tools to communicate Balanced Scorecard information.

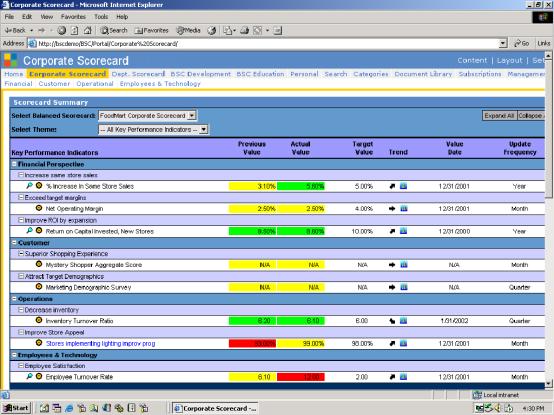

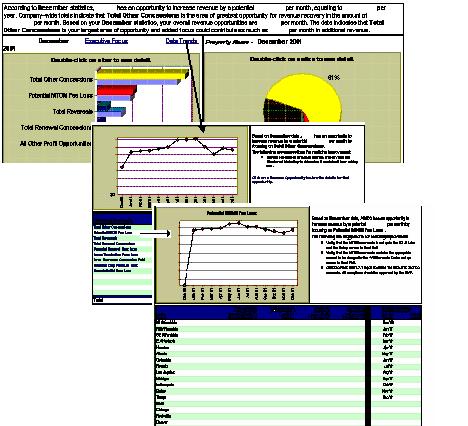

First among these presentation tools is the scorecard summary, called Scoreboard™, which shows at a glance the critical information relative to each perspective, objective, and measure. The Scoreboard can be filtered by theme or set to display all corporate measures. Information presented includes current and previous values, targets and trends of measures, comments, and links to analysis so that a viewer may answer questions readily. Color and graphics are used to convey whether a measure is on target or needs attention.

Second, the strategy map is included to show a graphical explanation of the perspectives, objectives, measures, and the causal relationships. The strategy maps can be viewed in conjunction with the scorecard itself, and are interactive, allowing users to switch between themes and click on any element (including the cause and effect links) to view additional information.

Third, a sub-dashboard for each perspective contains information relevant to that perspective. Here, the strategy matrix for each perspective is presented. The sub-dashboards also contain detailed information and additional measures that are not included on the summary scorecard.

Regardless of whether a viewer is looking at information on a strategy map, scorecard summary, or strategy matrix, hyperlinks permit access to the detailed information on any scorecard element.

Figure

5:

Scoreboard

Facet 4: Business Intelligence

Scorecards—balanced

or otherwise—are about improving performance. However, though scorecards point

to critical problem areas that need analysis, they do not perform that analysis

or indicate what action must be taken. In many cases, the scorecard will include

measures that are highly aggregated, and derived from multiple data points. For

example, if on-time delivery is below the targeted levels, corrective action is

predicated on analysis to determine which products, facilities, suppliers or

circumstances are primarily responsible for the delays. In other cases, an

average measure across multiple facilities may include both excellent performers

and poor performers, so drilldown is needed to make improvements.

Scorecards—balanced

or otherwise—are about improving performance. However, though scorecards point

to critical problem areas that need analysis, they do not perform that analysis

or indicate what action must be taken. In many cases, the scorecard will include

measures that are highly aggregated, and derived from multiple data points. For

example, if on-time delivery is below the targeted levels, corrective action is

predicated on analysis to determine which products, facilities, suppliers or

circumstances are primarily responsible for the delays. In other cases, an

average measure across multiple facilities may include both excellent performers

and poor performers, so drilldown is needed to make improvements.

Of course,

not all measures are conducive to this type of “drill-to-detail” analysis.

However, for those that are, a range of business intelligence tools exists to

provide this analytic capability. The Balanced Scorecard links to sources of

detailed information, with different types of analyses for different users. Some

situations require specific, targeted analyses. Others require a more general

framework for “ad hoc” analysis. The Scoreboard includes graphical

indicators (magnifying glass for ad hoc and target for targeted) to cue the

users to which types of analyses are available for a given measure.

Figure 6:

Ad Hoc Analysis

Analytic capabilities are critical to improving performance by providing information that people can use to make decisions, that is, “actionable insights.” The end goal of analysis is performance improvement through action, so there is a natural link between analysis and tools that prompt and facilitate action.

Facet 5: Actionable and Operational Tools

Actionable

and operational tools are the tools used to facilitate action, because success

depends on equipping people with the means to improve their performance.

For instance, in the case of on-time delivery, part of the solution may be to

deploy an early warning system that can help to address potential delivery

problems before the shipment is late.

Actionable

and operational tools are the tools used to facilitate action, because success

depends on equipping people with the means to improve their performance.

For instance, in the case of on-time delivery, part of the solution may be to

deploy an early warning system that can help to address potential delivery

problems before the shipment is late.

The BSCF exploits a powerful synergy between measurement tools, which motivate people, and operational tools, which empower people to make improvements. Examples can include exception reports, automated alerts, and linking to transactional systems in order to reduce the time between problem recognition and resolution.

Actionable and operational tools may also include functionality from Enterprise Resource Management, Customer Relationship Management, or other operational systems that can be included in the portal to facilitate transitions between analytic and operations tasks.

Actionable tools can also be designed to tell people what to do, which is important in a decentralized company with people at numerous levels, all taking action based on scorecard information. In the targeted analysis below, note:

Information is provided in context so people understand their relationship to the whole organization.

Both graphic and numeric styles of communication are integrated to accommodate different learning styles.

Context-sensitive help guides users to exactly what they must do for success, resulting in a set of actionable instructions arising from analysis.

Figure 7: Targeted Analysis Blended with Actionable and Operational Tools

Knowledge

management capabilities facilitate many aspects of the Balanced Scorecard

process

Knowledge

management capabilities facilitate many aspects of the Balanced Scorecard

processFirst, knowledge management implies keeping track of the multitude of documents generated in an organization. SharePoint Portal Server provides a repository, like an electronic library, so documents can be accessed readily by all authorized people. Useful document management features include:

Security, so only authorized people can view a document.

Search capability, so people can find documents based on criteria like author, date published, topic, or key words.

Version control, to make sure change history is captured and that all people access the latest version of a document.

Indexing, or the ability to make an electronic catalog of existing documents for inclusion in the library.

Subscription, so people can be automatically notified if documents change.

Of course, this functionality is not just used for Balanced Scorecard information, but also for a range of corporate documents, including process control documents, product development information, price lists, human resources policies and procedures, and so on. In some cases, these robust, document-handling features are required to support initiatives like ISO 9000:2000 certification.

Second, knowledge management includes collaboration. Because knowledge workers do not operate in isolation, collaboration is vital. Collaboration means being able to share, route, and discuss documents within and among levels of an organization. Collaboration applies equally to scorecard development at the executive level, to cascading the scorecard through levels of a company, and to ongoing scorecard evaluation. Tools of collaboration include on-line net-meetings, threaded electronic discussions, and automated workflows to route documents for approval. These collaboration tools help provide a return on knowledge workers by speeding productivity, and help weave the balanced scorecard into busy workdays.

Of course, as

with document management, collaboration tools are extremely useful to all

aspects of knowledge work.

Figure 8:

Search Capabilities of SharePoint Portal Support the Balanced Scorecard

A Balanced Scorecard initiative represents a watershed event in an organization’s evolution. It is a challenging, inter-disciplinary process of cultural change. To be successful, an organization needs a defined, multi-faceted approach that embraces education, communication, scorecard development, and ongoing implementation. The Microsoft Balanced Scorecard Framework meets these criteria.

Figure 9:

The Microsoft Balanced Scorecard Framework

The Microsoft approach to Balanced Scorecard automation brings together:

Portal technology to facilitate education, change, and communication.

Information on best practices from Balanced Scorecard experts.

Strategy and metric management in conformance with the specifications put forth by the Balanced Scorecard Collaborative, the consulting organization founded by the creators of the Balanced Scorecard.

Analytic capabilities to bridge the gap between problem identification, as shown by out-of-tolerance measures, and analysis, to determine underlying opportunities for performance enhancement.

Actionable and operational tools to enhance and work in conjunction with business intelligence tools.

Knowledge management to permit sharing and control of documents, on-line collaboration, work flow, and document searching.

Organizations

seeking to implement a Balanced Scorecard are striving to become a strategy

focused organization. Strategy focused organizations exploit the Balanced

Scorecard and technology to become more agile. These organizations attain

incremental returns on their customers, processes, employees, and technologies.

The Microsoft Balanced Scorecard Framework delivers these returns in a

cost-effective, reliable, scalable manner.

The

Balanced Scorecard - Measures That Drive Performance,

Kaplan, Robert S., and Norton, David P.;

Article, Harvard Business Review,

January 1992.

Putting

The Balanced Scorecard To Work,

Kaplan, Robert S., and Norton, David P.;

Article, Harvard Business Review, September 1993.

Using the

Balanced Scorecard as a Strategic Management System,

Kaplan, Robert S., and Norton, David P.;

Article, Harvard Business Review, January-February 1996.

The

Balanced Scorecard: Translating Strategy into Action,

Kaplan, Robert S., and Norton, David P.;

Harvard Business School Press, 1996.

The

Strategy Focused Organization,

Kaplan, Robert S., and Norton, David P.;

Harvard Business School Press, 2001.

Having

Trouble With Your Strategy? Then Map It,

Kaplan, Robert S., and Norton, David P.;

Article, Harvard Business Review, September-October 2000.

Balanced Scorecard Institute home page http://www.balancedscorecard.org

Contact

Michelle C.

Wing

[email protected]

The information contained in this document represents the current view of Microsoft Corporation on the issues discussed as of the date of publication. Because Microsoft must respond to changing market conditions, it should not be interpreted to be a commitment on the part of Microsoft, and Microsoft cannot guarantee the accuracy of any information presented after the date of publication.

This

white paper is for informational purposes only. MICROSOFT MAKES NO WARRANTIES,

EXPRESS OR IMPLIED, IN THIS

DOCUMENT.

Complying with all applicable copyright laws is the responsibility of the user. Without limiting the rights under copyright, no part of this document may be reproduced, stored in, or introduced into a retrieval system, or transmitted in any form or by any means (electronic, mechanical, photocopying, recording, or otherwise), or for any purpose, without the express written permission of Microsoft Corporation.

Microsoft may have patents, patent applications, trademarks, copyrights, or other intellectual property rights covering subject matter in this document. Except as expressly provided in any written license agreement from Microsoft, the furnishing of this document does not give you any license to these patents, trademarks, copyrights, or other intellectual property.

© 2001 Microsoft Corporation. All rights reserved.

The example companies, organizations, products, domain names, e-mail addresses, logos, people, places, and events depicted herein are fictitious. No association with any real company, organization, product, domain name, e-mail address, logo, person, place, or event is intended or should be inferred.

Microsoft, PowerPoint, and SharePoint are either registered trademarks or trademarks of Microsoft Corporation in the United States and/or other countries.

The names of actual companies and products mentioned herein may be the trademarks of their respective owners.Visit the Authors Web Site

Search Our Site

Search Our Site

Search the ENTIRE Business

Forum site. Search includes the Business

Forum Library, The Business Forum Journal and the Calendar Pages.

Disclaimer

The Business Forum, its Officers, partners, and all other Home

Calendar The Business Forum Journal

Features

Concept

History The Business Forum webmaster:

bruceclay.com

parties with which it deals, or is associated with, accept

absolutely no responsibility whatsoever, nor any liability,

for what is published on this web site. Please refer to:

Library

Formats

Guest Testimonials

Client Testimonials

Experts Search

News Wire Join

Why Sponsor

Tell-A-Friend

Contact The Business Forum

9297 Burton Way, Suite 100

Beverly Hills, CA 90210

Tel: 310-550-1984 Fax: 310-550-6121

[email protected]